Target Date Fund Pros and Cons: The Risks of Excessive Caution

July 19, 2023 July 19, 2023 /

When evaluating investment options that suit your specific financial circumstances and aspirations, it is crucial to consider Target Date Fund (TDFs) pros and cons. These funds have gained prominence in the realm of retirement planning due to their seemingly straightforward and hands-off approach.

However, before making any decisions, it is essential to delve into the advantages and disadvantages associated with TDFs. By carefully weighing the benefits and drawbacks, you can make a well-informed choice that aligns with your long-term financial goals.

On closer inspection, this one-size-fits-all strategy presents its own challenges, including a balance of benefits and potential disadvantages.

While TDFs offer a simplified solution for investment, their performance, when juxtaposed with broad market index funds, often falls short.

This disparity in returns can significantly impact your timeline to financial independence, potentially necessitating additional working years to reach your retirement savings goal.

Therefore, it’s crucial to delve into the intricacies of TDFs and consider whether this seemingly straightforward investment approach aligns with your long-term objectives for a secure and timely retirement.

What is a Target Date Fund (TDF)?

TDFs, sometimes known as lifecycle or age-based funds, are mutual funds that adjust the asset allocation based on your specified retirement date. As the target date approaches, the fund’s risk profile decreases, shifting from aggressive to more conservative investments.

Advantages of Target Date Funds

Simplified Investing

TDFs take the guesswork out of investing, providing a single investment solution tailored to your retirement timeline. They eliminate the need to periodically rebalance your portfolio, an activity that requires time, knowledge, and commitment.

Diversification

A TDF provides you access to a wide range of asset classes, including domestic and international stocks, bonds, and sometimes, real estate and commodities. This diversification helps to spread out risk and could potentially enhance returns.

Automatic Rebalancing

As you move closer to your retirement date, the fund’s focus shifts from growth to capital preservation. TDFs automatically adjust their asset allocation, reducing your exposure to volatile markets as you near retirement.

Disadvantages of Target Date Funds

One-Size-Fits-All Approach

TDFs base their investment strategies on the anticipated retirement date, not taking into account your risk tolerance, financial circumstances, or other personal factors. Therefore, the fund may be too conservative or too aggressive for your unique situation.

Lack of Control

Investing in a TDF means giving up control over individual investment choices. If you prefer having a hands-on approach to your investment portfolio, a TDF may not be the right choice.

Potential for Higher Fees

TDFs often have higher expense ratios compared to other mutual funds. These fees can eat into your investment returns over time, potentially making a significant difference in your retirement savings.

Is a Target Date Fund Right for You?

Whether a TDF is the right choice hinges on your investment knowledge, time, and comfort with risk. If you’re seeking simplicity and automatic adjustments as you age, a TDF may be an excellent fit. However, if you prefer more control over your investments and have a unique risk profile, exploring other options may prove beneficial.

Weigh the pros and cons, evaluate your financial situation, and make an informed decision. A carefully chosen investment strategy is a significant step towards a financially secure retirement.

Comparing Target Date Funds and Index Funds

The investment landscape offers a variety of tools, each with its unique advantages and intricacies. Two such tools that often garner attention from investors are Target Date Funds (TDFs) and Index Funds. This section delves into the distinguishing features of both, helping you better understand which might best align with your financial goals.

Understanding Index Funds

Index Funds are a type of mutual fund or Exchange-Traded Fund (ETF) constructed to mirror or track the components of a financial market index, such as the S&P 500. They offer a passive investment strategy, aiming to replicate market performance, unlike active funds that try to outperform the market.

Note: Passive Index Fund investing is a popular method used by many in the financial independence community for long-term wealth building.

Benefits of Index Funds

Broad Market Exposure

By replicating an index, these funds offer exposure to a wide range of companies, diversifying your portfolio and helping mitigate risk.

Lower Costs

Index Funds typically come with lower expense ratios as they employ a passive management strategy. Lower costs translate into more of your money working for you, which can significantly impact long-term investment returns.

Transparency

The holdings of an Index Fund are publicly available and updated regularly. This transparency allows you to know exactly where your money is invested.

Limitations of Index Funds

No Potential for Outperformance

Since Index Funds aim to mirror market performance, they don’t strive to outperform the market. In bullish market conditions, you won’t reap extra benefits.

Don’t worry about this. You are a smart person but you likely won’t beat the market over time. Focus on the things you can control like how aggressive you invest and the market average returns (8-10%) will serve you just fine.

Lack of Flexibility

Index Funds’ objective to match a particular index leaves little room for flexibility. Fund managers can’t adapt the portfolio to changing market conditions.

Again, don’t worry about this. We are okay with average market returns. We just make this assumption in our planning and continue to invest assertively.

TDFs vs. Index Funds: Key Differences

Investment Strategy

While TDFs offer a set-and-forget strategy that adjusts with your age, Index Funds provide a static investment strategy, mirroring a particular market index.

Risk Profile

TDFs aim to reduce risk as the target date approaches, shifting from more volatile investments (like stocks) to more conservative ones (like bonds). On the other hand, the risk profile of an Index Fund is contingent on the makeup of the underlying index.

Cost Structure

Generally, TDFs have higher expense ratios due to their active management style, while Index Funds are often more cost-effective due to their passive strategy.

Making an Informed Decision

TDFs and Index Funds, each with their distinct advantages and drawbacks, cater to different investor needs. If you’re looking for a hands-off, age-adjusted retirement investment, a TDF could be the right choice. However, if you prefer a cost-effective, passive investment tool, you might lean towards Index Funds.

Investing is not a one-size-fits-all journey. It’s about understanding your financial goals, risk tolerance, and personal circumstances, and then aligning these factors with the right investment tools. Always remember to research thoroughly and consult a financial advisor if necessary.

Target Date Fund vs. Index Fund

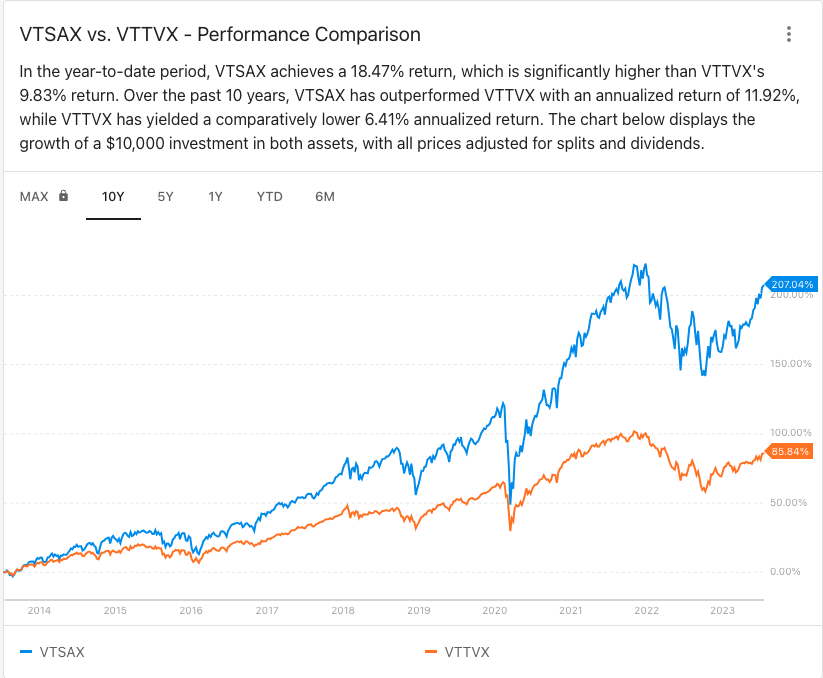

VTTVX vs VTSAX

Consider the following information in your decision. You may not be so eager to invest in TDFs.

Let’s take a look at Vanguard’s Target Retirement 2025 Fund (VTTVX) vs Vanguard’s Total Stock Market Index Fund Admiral Shares (VTSAX). VTSAX is a financial independence community favorite for wealth building. It is classified as a broad market low cost index fund. In this case, not only did VTSAX considerably outperform the 2025 TDF, the expense ratio is about half that of the 2025 TDF, keeping more of your hard earned money working for you.

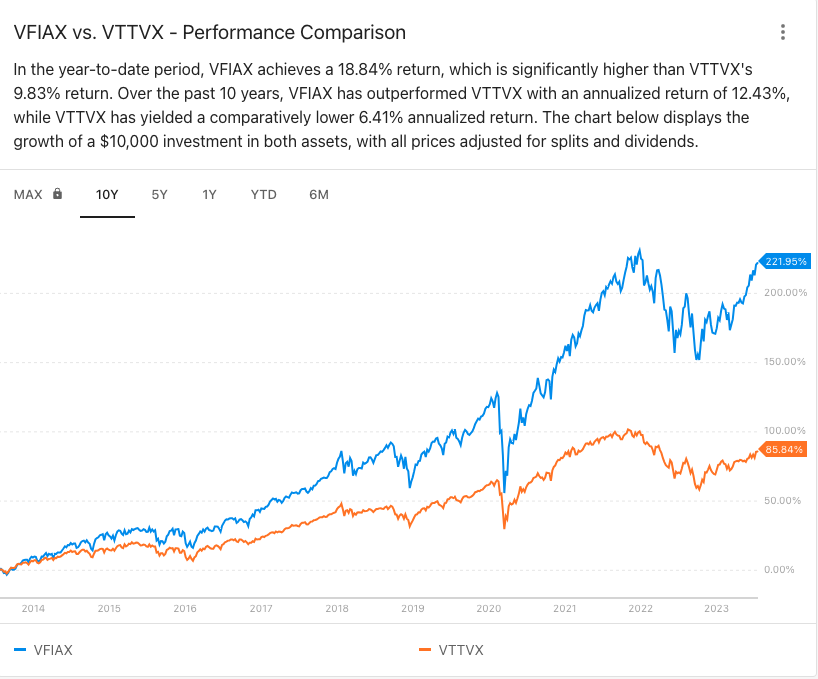

VTTVX vs VFIAX

If you make contributions to your 401k and VTSAX is not available as an option, it is probable that you have access to an S&P 500 Index Fund. When comparing the performance between Vanguard’s Target Retirement 2025 Fund (VTTVX) and Vanguard’s S&P 500 Fund (VFIAX), note that while the peaks and troughs are more significant in VFIAX (Index Fund) but in the end it still convincingly outperformed VTTVX (TDF).

Considering the pros and cons of Target Date Funds, it’s important to reflect on your current investment in these funds. While it may give you a sense of security knowing that the fund automatically adjusts over time to become more conservative, it’s essential to recognize that this approach might cause you to miss out on potentially better performance.

If your company doesn’t offer a low-cost broad market index fund, I encourage you to reach out to your HR department and request its inclusion. While your retirement program may be managed by a third-party administrator, they would likely prefer to accommodate your request rather than risk losing your company’s business to another investment firm that can meet your needs.

The bottom line is this: if you are currently invested in a Target Date Fund, carefully consider whether the tradeoff is truly worthwhile. Historically, opting for a broad market index fund has shown significantly better long-term performance, despite the higher volatility. If you automate your monthly contributions and seldom check your balance, why not aim for higher returns? Doing so might enable you to reach your financial goals and potentially retire years earlier than anticipated.

What if I No Longer Want to Deal With Market Fluctuations?

If you determine that you need more stability in your portfolio as retirement approaches, you can easily transition shares of your index fund into an appropriate bond fund. These funds often have lower fees and can achieve similar outcomes to the final stock-to-bond mix of a Target Date Fund

Conduct thorough research and explore the available options within your employer’s retirement plan. If you find that certain offerings are not aligned with your needs and the needs of your coworkers, don’t hesitate to request changes to better suit your long-term goals.

These principles apply not only to investing in employer-sponsored plans but also to investing in your own taxable brokerage account.

While the examples provided above showcase Vanguard funds, it’s worth noting that major fund families such as Fidelity, T. Rowe Price, BlackRock, and Charles Schwab offer similar investment options with comparable performance.

Reconsidering the Trade-Off: Evaluating Target Date Fund Pros and Cons

When it comes to selecting funds or managing your portfolio, you may find yourself lacking confidence or knowledge. Perhaps your initial introduction to investing through your HR department emphasized the benefits of Target Date Funds, highlighting their gradual shift towards a more conservative approach over time, intended to protect your investments.

While this approach may hold true if you constantly react to market fluctuations, constantly entering and exiting positions, it falls short when considering a committed long-term investment strategy. Investing is ultimately about maximizing returns to secure the lifestyle we desire in the future.

Take a moment to revisit the comparisons outlined in the analysis of Target Date Fund pros and cons. Will you be content knowing that your retirement savings could potentially be significantly diminished due to your choice of a Target Date Fund, rather than embracing the volatility of the market and its potential for growth?